Consumer debts – new legislation

The new legislation on consumer debts and its implementation will probably come into force this year. This will require an adjustment from many companies. We go through the most important points below to make sure that you are completely up to date.

Book XIX consumer debts

On April 27, 2023, “de Kamer” adopted a new bill in a second reading. The law is now presented before the King for endorsement. It will enter into force on the first day of the 4th month after its publication in the Belgian Official Gazette. So we can’t give an exact date yet. Perhaps this will take place at the end of 2023.

What’s new pussycat?

This law will be adding a new book to the Economic Law Code (Wetboek Economisch Recht, WER). This book is divided into two windows. The first title will be about the payment of debts from the consumer to a business in general. The second title will be about the amicable collection of it. The old Law of 20 December 2002 (on amicable recovery) is included here in an adapted version.

Application

This is important to clear up: it only concerns debts of a consumer or private individual to a company and amicable collection. So without an enforceable title, such as a judgment.

First reminder for free

As an company, you will first have to provide your customer with a free reminder. You must take a payment term of at least 14 days into account. This term only starts – when sent by paper mail– on the third working day after the shipment. So you have to take into account a total of 17 days. If you send your message via e-mail, the term starts the day after it is sent.

As mentioned, you may not immediately charge costs. If you have a long-term contract in which you regularly supply (e.g. energy), you will have to provide three free reminders on an annual basis. Afterwards you may charge costs up to a maximum of 7.50 euros plus the actual postage costs.

Interest on late or late payment

Does the consumer not respond to the reminder? In this case you can claim interest. You must of course record this contractually, for example in the general terms and conditions. You can apply the interest retroactively from the day after the first reminder was sent. This last rule only applies to SMEs.

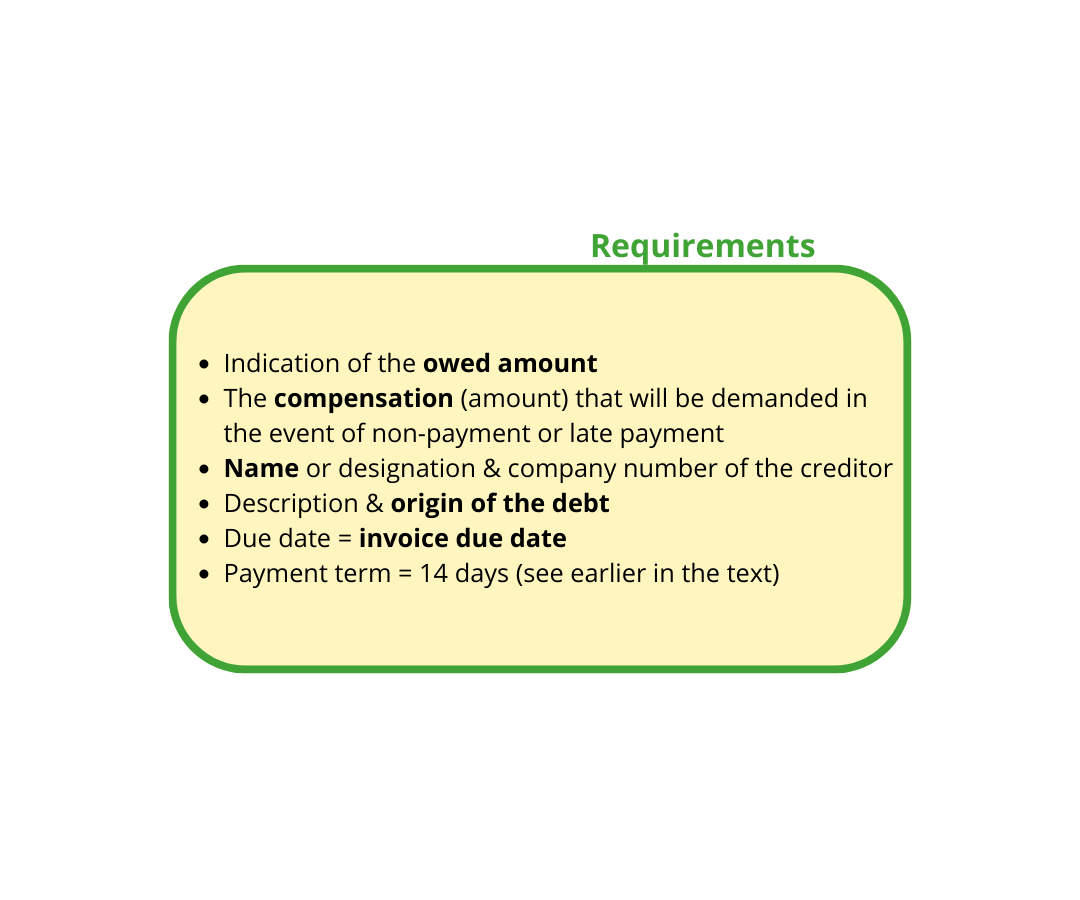

Compensation

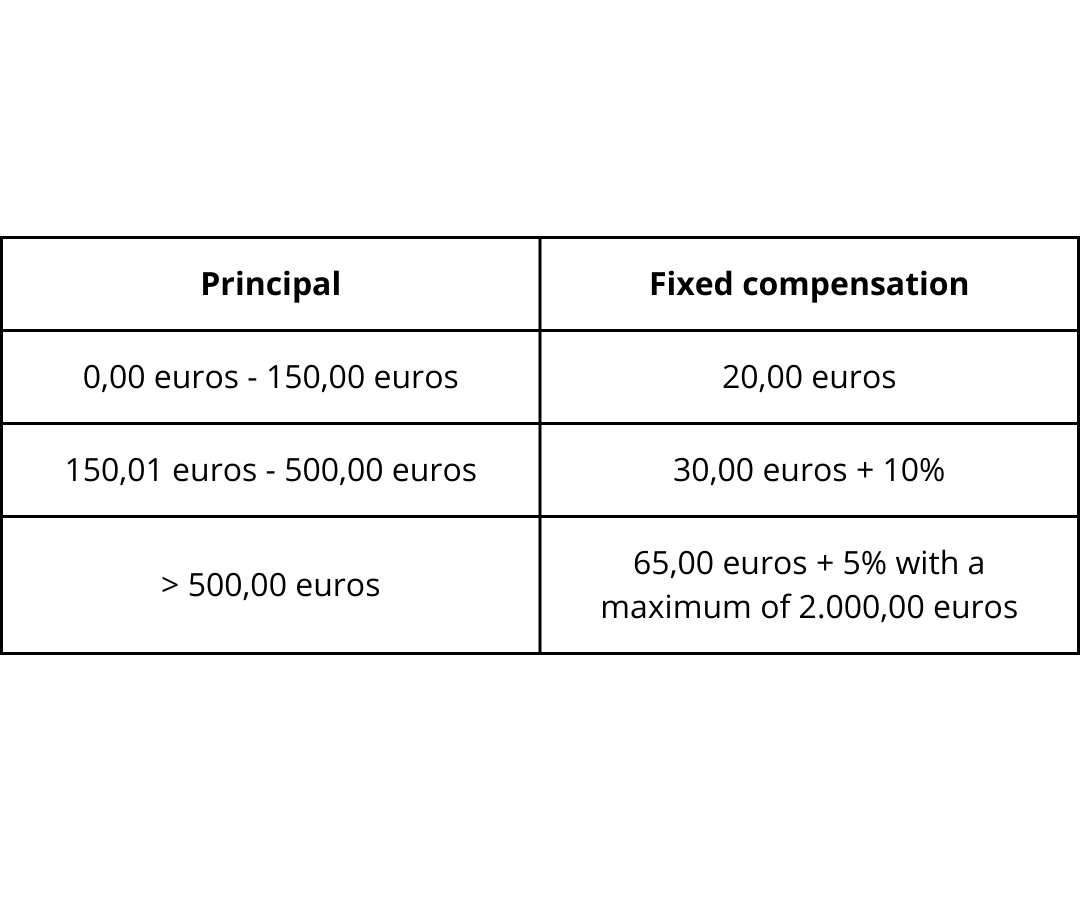

You can claim compensation in one of two ways. Via a simple interest rate as mentioned above. This is then a maximum of the reference interest rate, increased by 8%. The other possibility is, thta you can work with a fixed compensation. The legislature has set limits on this.

Title 2: amicable recovery

The original Act of 20 December 2002 can be found in an adapted form in the WER. We only provide the changes and the most important points for attention.

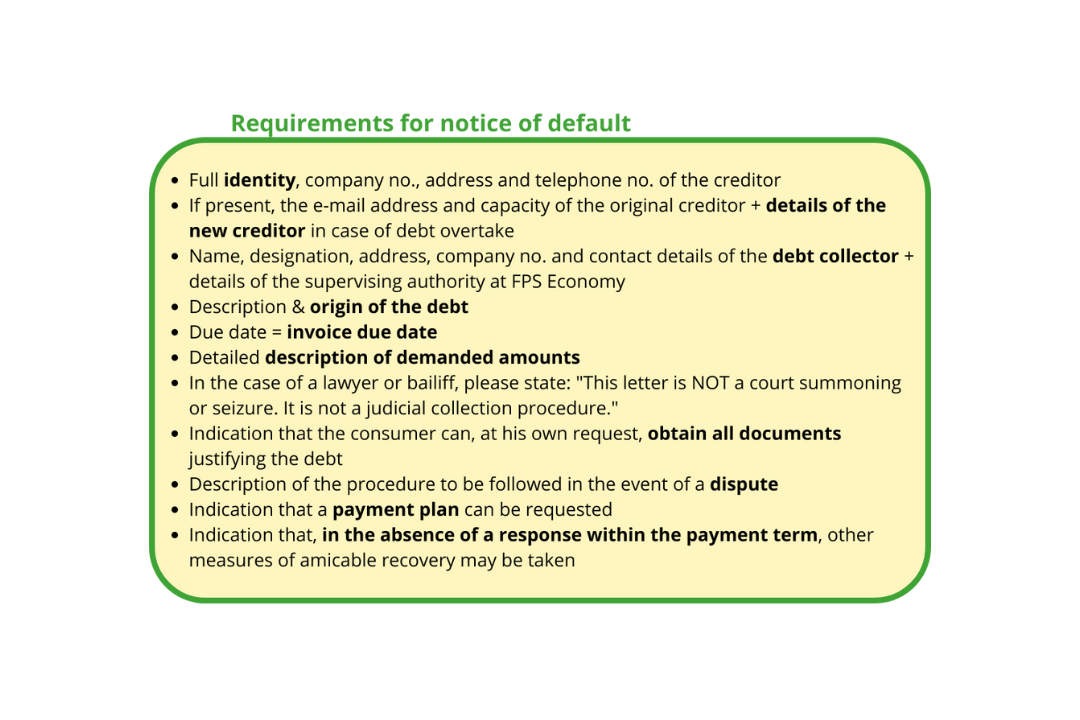

Prohibited measures

You may not take any other measures or perform any actions before you have sent a notice of default. This means that SMS messages, telephone calls, … are now also completely equal.

Payment plan or dispute

When the consumer requests a payment plan or submits a reasonable dispute, you may temporarily not take any other measures or perform any actions. This is ongoing until the decision on the plan or dispute has been announced. If this decision is delayed for more than thirty days, the interest will stop running.

If you have assigned a payment plan, you will have to provide a state of affairs to your private customer at least once a year. When the plan expires, you are obliged to communicate about this.

Amicable debt mediation or collective debt settlement

As soon as the consumer submits an application for amicable debt mediation or a petition for collective debt settlement, you are not allowed to take any measures or perform actions for collection. This temporary ban runs for a period of 45 days, counting from the application or submission of the petition.

Transitional provision

This new legislation will also already apply to contracts concluded before the implementation, under the condition that the debt matures after this date. In other words: the expiry date is decisive.

Concerns

1 The general aim of the legislator is noble: additional consumer protection. That may be necessary. It remains to be seen whether these rules meet this requirement. An example of this is the energy sector. Many specific provisions already apply therein. These new rules now come on top of that. This may create legal uncertainty.

2 The payment term is being extended from 15 to 17 days, while the same legislator has shortened the payment term in B2B cases at the beginning of 2022.

3 The free reminder can provide a certain amount of reassurance for private individuals. They know that they have a little longer to pay, without additional costs. As a result, the working capital of our companies may experience pressure.

TIP: you will have to adjust your administration. Think about agreements, general terms and conditions, collection procedures and templates. Don´t wait too long, because autumn may arrive sooner than expected.

Stay in touch!

Sign up for our newsletter and get access to:

- The latest news about iCredit

- Available finance consultants

- Personal invitations to our events

- Free access to our webinars